June Rate Strategy

Market Overview — June 2026

The Reserve Bank held the OCR at 2.25% last week — but only just. The Committee split 3-3 and the Governor’s casting vote was needed to hold. The new track signals the first hike in September, with the OCR projected to peak around 3.3% in 2028.

So rates didn’t move this month, but the Bank is sitting much closer to hiking than holding. And clients are asking the same question: which fixed rate should I choose?

What stands out in the data is how far apart the bank economists are on where the OCR ends up. ANZ has it peaking at 3.00%. BNZ peaks at 4.00%, and Westpac at 4.25% before easing back to 3.75% neutral by 2030.

Why are bank economists so far apart? They’re trying to weigh up a stagflation problem — prices rising sharply on one side, growth weakening on the other. The Iran war is feeding through to higher fuel and energy costs, and the RBNZ now expects inflation to peak at 4.3% later this year — well above the top of its 1–3% target band. The bigger concern is whether that pressure broadens into wages and other domestic prices. At the same time, growth is weak. The Bank’s GDP forecast for the year to March 2027 has been cut from 2.8% down to 1.7%, with household budgets squeezed by higher fuel bills. The hawkish camp (BNZ, Westpac) argues the RBNZ has to hike sooner and further to anchor inflation expectations. The dovish camp (ANZ, Kiwibank) thinks the economy is too soft for much tightening. Both have a fair argument behind them.

Mortgage rates over the next 6–12 months

The banks forecast the OCR; we translate those paths into expected mortgage rates. Across the six tracks, the OCR is projected to rise 75–175bp over the next 12 months (3 to 7 hikes).

Variable (today 5.81%, moves with the OCR): full pass-through puts it between roughly 6.55% (dovish view) and 7.55% (hawkish view) in 12 months. Banks will likely compress some of the currently wide variable margin as the cycle progresses, softening the move. Customers on variable can usually negotiate 50–100bp off carded.

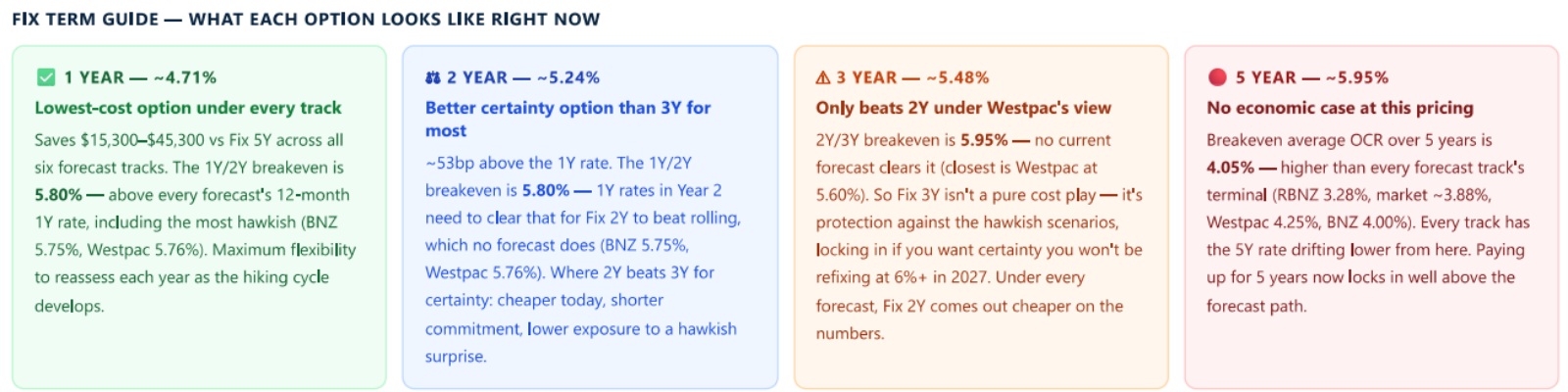

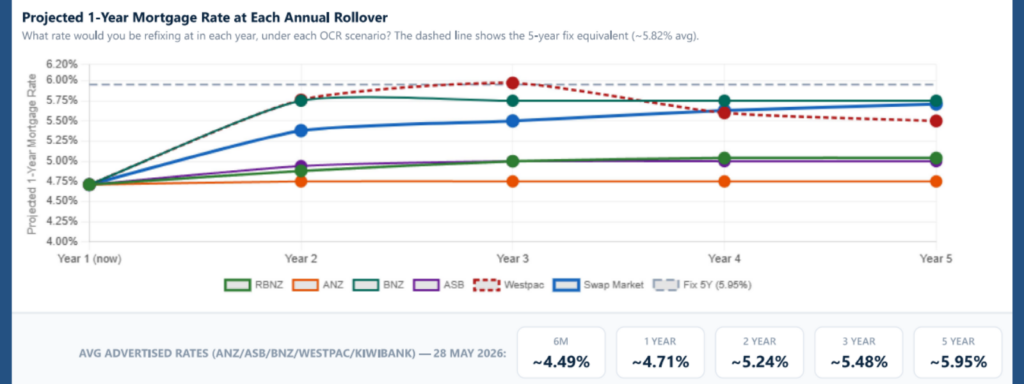

1-year fixed (today 4.71%): expected range 5.00–5.80% at 12 months. Central case around 5.35%.

2-year fixed (today 5.24%): expected range 5.10–6.00% at 12 months. Central case around 5.55%.

A note on bank margins. Carded fixed rates have compressed relative to underlying swap rates over the past six months, but banks have been rebuilding margin at the long end again over May. Even if wholesale rates ease from here, 3- and 5-year carded rates may stay sticky as banks defend that margin.

So what to do with your fixed rate decision

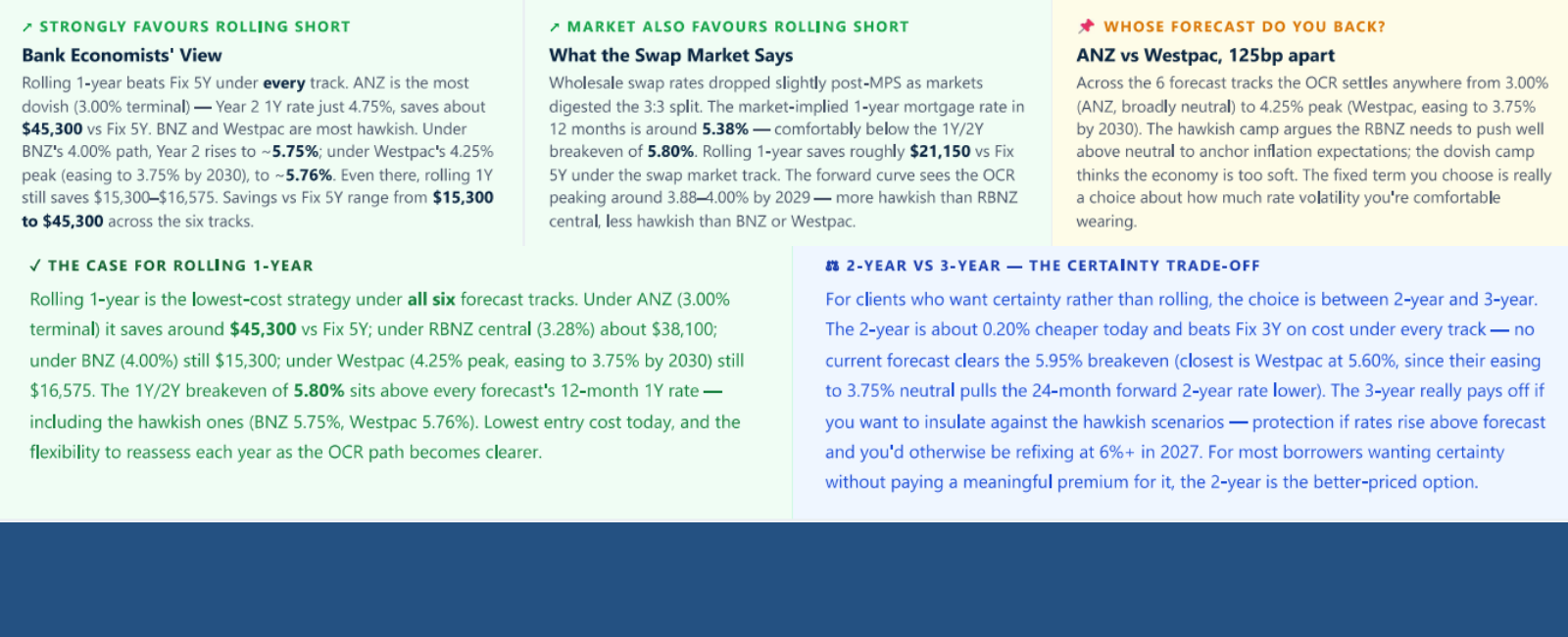

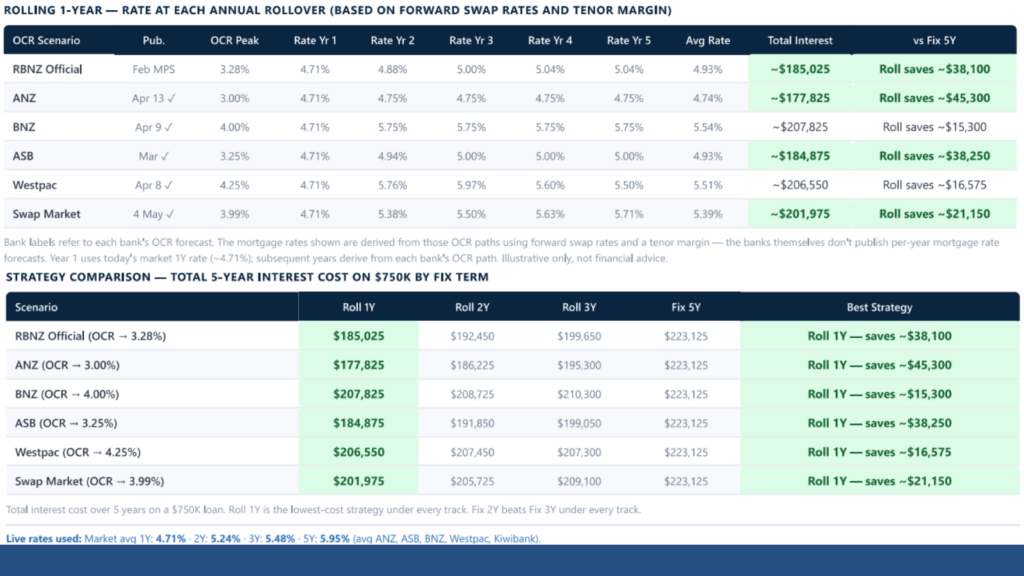

On the numbers, rolling the 1-year is the cheapest option under every forecast. The 1Y/2Y breakeven is 5.80% — the rate the 1-year would need to clear in 12 months for a 2-year fix today to come out ahead. No forecast clears it (closest is Westpac at 5.76%). If cost is your only criterion, roll the 1-year.

For borrowers wanting certainty rather than chasing the lowest cost, the question is 2-year or 3-year. The case for 3 years comes down to your appetite for rate volatility. Given the wide range of forecast outcomes, fixing for 3 years might make sense if you want to protect against the possibility of rates being 6% or higher in two years’ time when a 2-year fix would otherwise roll off.

The 2Y/3Y breakeven is 5.95% — and no current forecast clears it. The 2-year is also about 0.20% cheaper than the 3-year today, and the 2-year strategy comes out ahead on cost under every track.

In short — want lowest cost and flexibility? Roll the 1-year. Want some certainty at a fair price? Fix the 2-year. Want to insure against the hawkish scenarios? Fix the 3-year.

This is a starting point, not a final answer. Your Income, your plans for the property, and your risk tolerance all matter. Worth talking through with your advisor.

OCR Forecast Paths

Key insights from June’s analysis

- The RBNZ delivered a hawkish hold on 27 May (3-3 vote, Governor’s casting decision). The first hike is now expected in September, with the OCR projected to peak around 3.3% in 2028 — earlier and higher than February.

- Bank economists disagree widely on where the OCR settles — anywhere from 3.00% (ANZ) to 4.25% (Westpac). The right fixed rate strategy depends on which view you back.

- Rolling the 1-year is the cheapest option under every forecast on the table. The breakeven would need the 1-year rate to clear 5.80% in 12 months, and no forecast track gets there.

- For borrowers wanting certainty, the 2-year is cheaper than the 3-year under every track except Westpac. The 3-year really pays off as protection against the hawkish scenarios — insurance against a 6%+ refix in 2027.

A few practical tips worth knowing

- This analysis uses advertised special rates. Your actual offered rate may be up to 20bps lower — that makes a real difference to the numbers.

- Use your bank’s rate lock. Usually free, often available 60 days before rollover — particularly useful with rates expected to drift higher.

- Think about your risk appetite. Could you manage comfortably if your rate hit 6%? Some certainty is worth paying for.

- Talk to an adviser about what’s right for your situation — general analysis can only take you so far.

- Don’t overlook refinancing. Cashback offers from new lenders can be significant (often $7,000–$9,000 on a $700K+ loan) and can meaningfully change the equation if you’re considering switching banks.

Disclaimer: This analysis is general information only and does not constitute personalised financial advice. All figures are illustrative, based on a $750,000 interest-only loan. Actual interest costs will vary with loan balance, repayment structure, rate timing and individual circumstances. OCR paths, forward rates and savings estimates are modelled scenarios, not predictions. Before making mortgage decisions you should seek advice from a financial adviser who can assess your specific situation and circumstances. Rupert Hunt is a New Zealand financial adviser.