July Rate Strategy

A month ago a July hike looked close to locked in and the question was how high rates might climb. The quick move to a ceasefire has changed that. Brent crude is back around US$73 a barrel, near where it sat before the conflict, and 91 unleaded has dropped to about $3.02 a litre, roughly 50 cents off its May peak. That feeds into a lower inflation track: the expected peak is back to about 4.0%, from 4.3–4.5% a month ago.

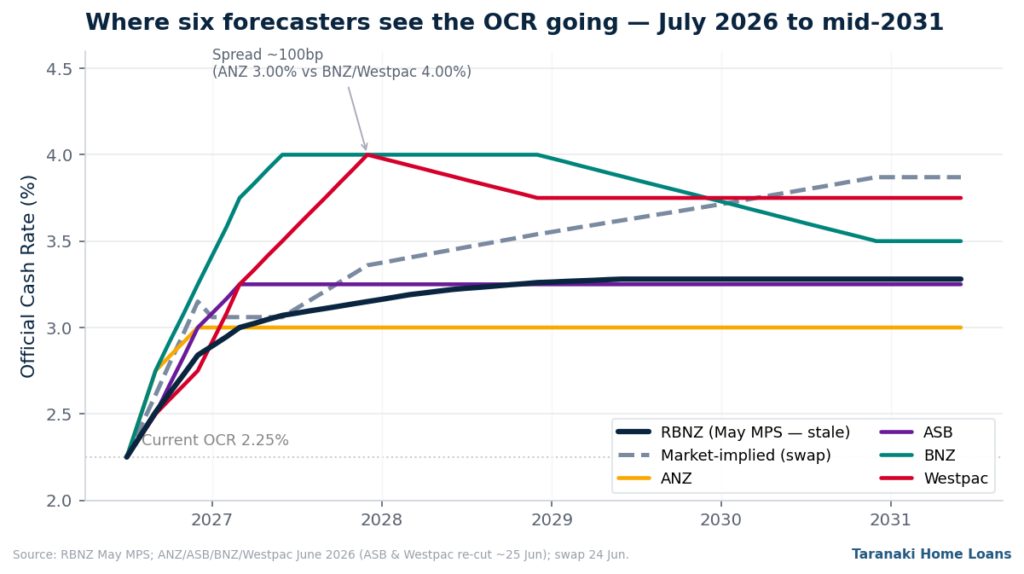

The economists are split on the 8 July decision. ASB and Westpac now expect a hold; ANZ and BNZ still expect a hike. That call matters less than where rates settle, and on that they broadly agree: still rising, but more slowly and to a lower peak than looked likely in May. For your refix, where rates settle counts for more than whether the first move lands in July or September.

Key takeaways

- Cheaper oil has eased the inflation outlook (peak now about 4%, down from 4.3–4.5%) and reduced the pressure on the Reserve Bank to hike.The 8 July decision is a close call: ASB and Westpac expect a hold, ANZ and BNZ a hike. It is an OCR Review, so no new Reserve Bank forecasts until the September MPS.

- Banks cut the long end of the carded curve through June: BNZ and Westpac are now 5.29% for 3 years and 5.49% for 5 years. ANZ has stopped offering 4 and 5-year specials.

- Our view: the OCR still rises, but slowly. Markets and several banks favour a July move; we think the oil fall may let the Reserve Bank wait until September. Either way, a gentle climb to near 3% rather than 4%.

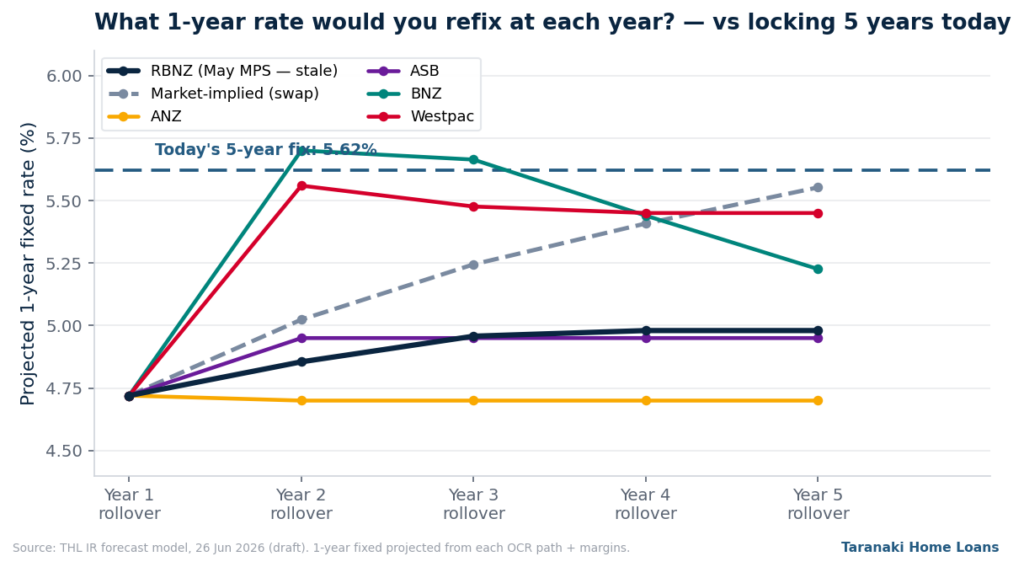

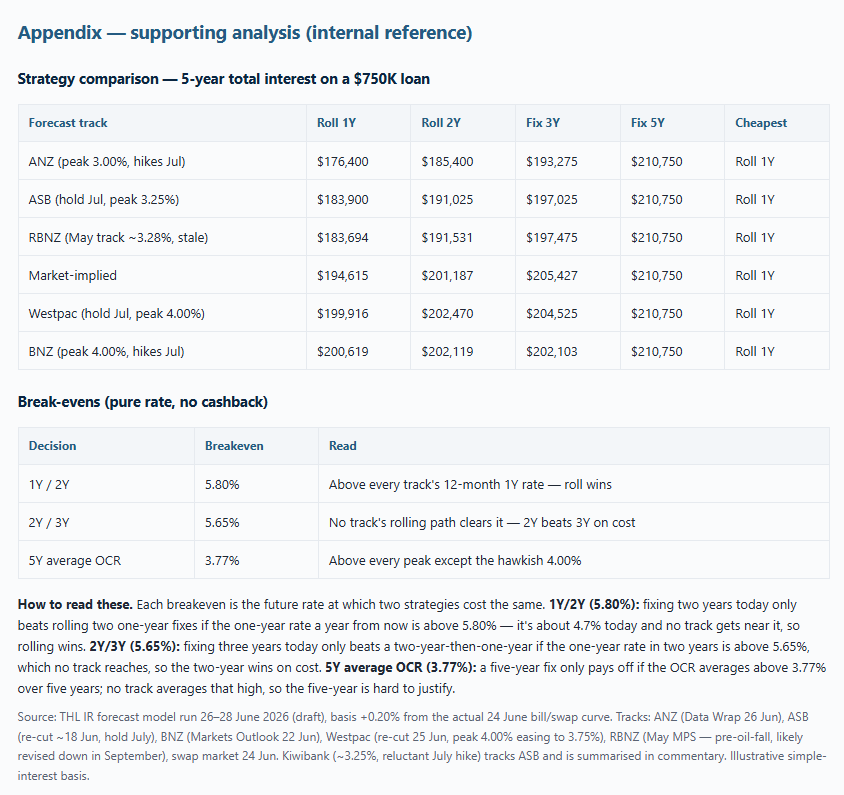

- Rolling the one-year is the cheapest option under every forecast — about $10,000 to $34,000 cheaper than a five-year fix on a $750K loan. The three-year is insurance, not a cost play.

What happened with mortgage rates this month

June was a busy month for advertised rates. ANZ lifted its fixed specials early in the month and SBS and TSB partly followed. Then swap rates fell as oil dropped, and the banks moved the other way: Westpac cut its three and five-year rates to 5.29% and 5.49% on the 19th, BNZ matched within days, and by the 24th ANZ had reversed its earlier rise and stepped out of the four and five-year market. The long end now sits well below where it started the month, while the one-year has barely moved.

The banks aren’t all in the same place, and the gaps are wide. BNZ and Westpac are sharpest at three and five years (5.29% and 5.49%), ANZ and ASB lead the one-year at 4.65%, and Westpac and SBS have the lowest two-year at 5.19%. Kiwibank and TSB are dearest at the long end, up to 5.99% for five years — about 50 points above BNZ and Westpac, or roughly $3,750 a year on a $750K loan. Which lender you are with matters as much as which term you choose.

| Tenor | Average Rate (Big 4 <80% LVR) |

|---|---|

| 6 Month | 4.64% |

| 1 Year | 4.72% |

| 2 Year | 5.26% |

| 3 Year | 5.39% |

| 5 Year | 5.62% |

ANZ has no 4 or 5-year special this month — those averages use the lenders still active at the long end.

What is influencing rates right now: the stagflation problem

Oil is the driver. Brent is back around US$73 a barrel and refined fuel has fallen further, which has taken roughly half a percentage point off the inflation outlook. The ceasefire is fragile and could come unstuck, but for now oil has held its falls. With the immediate inflation scare easing, the case for a pre-emptive hike on 8 July has weakened, and ASB and Westpac have moved to a hold.

ANZ and BNZ disagree. They argue cheaper fuel lowers near-term inflation but not the medium-term picture: the New Zealand dollar is weaker than the Reserve Bank assumed, and if lower fuel prices lift confidence and spending, one source of inflation simply replaces another. Their preference is to hike in July and keep their options open. Both views are reasonable. Either way, nobody is forecasting cuts; the question is only how far the OCR rises, and how fast.

Where we see rates heading over the next 6 to 12 months

We think the cash rate still rises, but slowly. Markets and several banks favour a first hike on 8 July; we think the drop in oil may let the Reserve Bank wait until September. Either way it’s a gentle climb — perhaps two hikes by Christmas — taking the OCR to about 2.75–3.00% by year-end and settling near 3% through 2027, rather than the 4% the more hawkish forecasts carry.

For mortgage rates over the next 6–12 months, that points to:

- One-year (4.72% today): up only modestly, toward about 5%.

- Two-year (5.26%): roughly steady.

- Three and five-year (5.29% / 5.49%):little further to fall. These had been priced too high for where the OCR is heading and have now corrected.

- Variable (around 5.62%):Unchanged until the Reserve Bank starts hiking.

The main risk is the ceasefire failing. If oil rises again, the banks will reprice up quickly.

Fixed versus floating considerations

Variable sits around 5.62% and moves with the OCR, so it won’t change until the Bank starts hiking, now more likely September than July. Most borrowers on variable negotiate below the carded rate, so the rate actually paid is closer to 5%.

| Term | Today | 12-month range | Central case |

|---|---|---|---|

| Variable | 5.62% | 5.50 – 6.25% | Rises once hikes start |

| 1-year | 4.72% | 4.70 – 5.70% | 5.00% |

| 2 Year | 5.26% | 4.80 – 5.90% | 5.20% |

The 3 and 5-year rates have already come down this month. With oil low and the inflation scare fading, the near-term pressure on the long end has eased — though a reversal in the Middle East remains the obvious risk.

What borrowers should consider if their rate is expiring

We compared four strategies on a $750K loan over five years, using each forecaster’s OCR path to project the rate you’d actually pay at each refix.

What this means for different borrowers

First-home buyers benefit from how keenly banks price the one-year, and the later-hike outlook gives a bit more breathing room. Rolling the one-year works on both cost and flexibility

Refinancers and people open to switching banks should look at cashback. Offers of $7,000–$9,000 on a $700K-plus loan can change the decision; just allow for the clawback if you switch again within a few years.

Existing homeowners staying with their current bank, the same one / two / three-year framework applies. There is less urgency now that a hike looks more likely in September than July, but it costs nothing to ask your bank for a rate hold while you decide.

Will the Reserve Bank hike on 8 July?

It’s genuinely split. After the fall in oil prices, ASB and Westpac now expect a hold; ANZ and BNZ still expect a 25bp hike. The 8 July decision is an OCR Review, so there won’t be a new forecast track that day — the next full update comes in September (2 Sept).

Will mortgage rates fall in 2026?

At the short end, not much — the 1-year is still expected to rise as the cash rate eventually lifts, just later than thought. At the long end, the 3 and 5-year rates have already fallen this month and could ease a little more if oil stays low. The big risk is a reversal in the Middle East.

Is now a good time to refix?

Rolling the 1-year is the cheapest option under every forecast, and the dovish shift has reinforced that. The 2-year is the middle-ground if you want some certainty; the 3-year only makes sense as insurance if you think the hawkish forecasts are right.

Should I choose a short-term or long-term fixed rate?

Short-term (1-year roll) is lowest cost and most flexible, and looks stronger after the oil-driven repricing. The 5-year is still hard to justify on the numbers.

What should I do if my fixed rate is expiring soon?

Ask your bank for a rate lock — usually free and available up to 60 days before rollover. Then work through the cost / certainty / insurance framework with your adviser, and compare against refinancing, where cashback offers are significant right now.

Closing section

Whether the Reserve Bank moves on 8 July or waits until September matters less than the direction: rates are rising more slowly, and to a lower peak, than looked likely a month ago. Rolling the one-year is still the cheapest option on every forecast we run. The two-year is the choice if you want certainty, and the three-year at 5.29% works as insurance if you think rates push to 4%. The five-year is hard to justify. The right answer depends on your situation — how much certainty is worth to you, and how a higher rate in a year or two would fit your budget — so talk it through with an adviser before you refix.

Taranaki Home Loans · July Rate Strategy (draft preview) · General information, not personalised financial advice. Rates are advertised special rates (<80% LVR) and your actual rate may differ. Talk to an adviser before making a decision.